साझा अर्थ संवाददाता

२८ असार २०८३, आइतवार

साझा अर्थ संवाददाता

२८ असार २०८३, आइतवार

Kathmandu, July 12, 2026

NEPSE recorded only one positive session during the July 6–10 trading week. Tuesday’s rebound was erased the following day, while the prominence of debentures in turnover rankings complicated the headline trading figures. SEBON’s promised capital-market roadmap has added a new source of expectation, but its impact will depend on implementation.

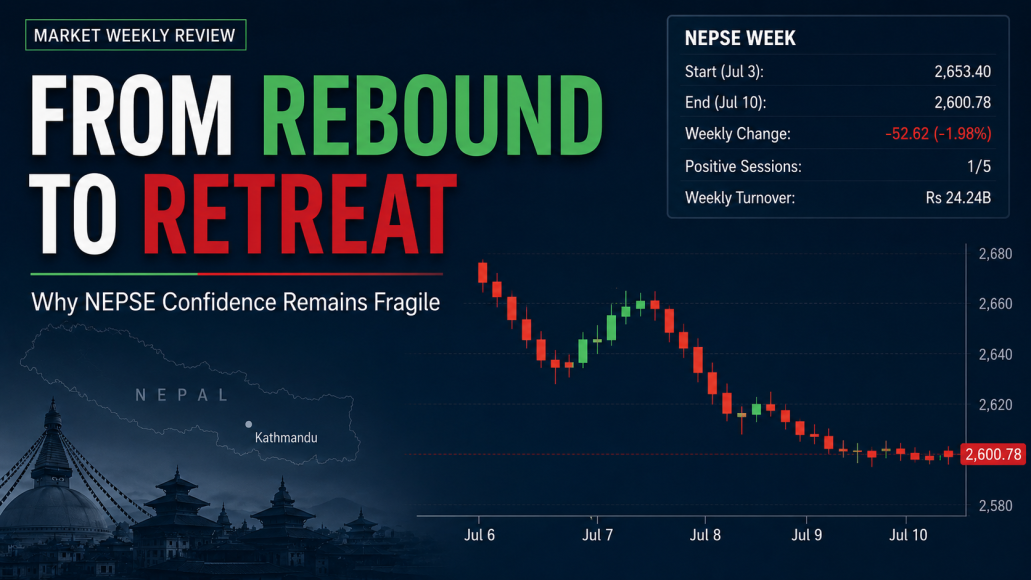

The Nepal Stock Exchange ended the July 6–10 trading week at 2,600.78, down 52.62 points, or 1.98 percent, from the previous Friday’s close of 2,653.40.

The benchmark recorded only one positive session during the week. A 24.57-point rebound on Tuesday was followed by a larger 30.09-point decline on Wednesday, after which the market continued to fall through Thursday and Friday.

The sequence highlighted the absence of sustained upward momentum. Although the index recovered most of Monday’s loss on Tuesday, the advance did not continue into the following session.

The weekly decline alone does not determine NEPSE’s longer-term direction. It does, however, show that the latest rebound lacked follow-through.

NEPSE opened the week with a decline of 26.29 points, or 0.99 percent, on Monday, closing at 2,627.11.

The index reached an intraday high of 2,661.46 but failed to retain the early gain. Total turnover stood at Rs 3.55 billion, while all sectoral indices closed lower.

The market reversed direction on Tuesday, gaining 24.57 points, or 0.93 percent, to settle at 2,651.68. Turnover increased to Rs 4.40 billion, and the index closed close to its intraday high of 2,651.86.

Tuesday was the only positive session of the week and recovered most of Monday’s decline.

The advance was erased on Wednesday.

NEPSE fell by 30.09 points, or 1.13 percent, to close at 2,621.59. The index ended below both Tuesday’s and Monday’s closing levels, while turnover increased to Rs 4.82 billion.

Higher trading activity therefore coincided with a falling index rather than an extension of Tuesday’s recovery.

The decline continued on Thursday, when NEPSE lost another 19.67 points, or 0.75 percent, and closed at 2,601.92. Turnover reached Rs 4.61 billion, and all sectoral indices ended in negative territory.

The index traded below 2,600 during the session before recovering slightly by the close.

Friday brought little change in the benchmark. NEPSE declined by 1.13 points, or 0.04 percent, to settle at 2,600.78. The index fell to an intraday low of 2,592.67 before closing slightly above the 2,600 mark.

Turnover increased sharply to Rs 6.86 billion.

The five sessions produced a simple pattern: a decline on Monday, a rebound on Tuesday and three consecutive negative closes from Wednesday to Friday.

Tuesday’s gain demonstrated the market’s capacity to rebound after a fall. Wednesday’s decline showed that the advance was not sustained.

Combined turnover during the five sessions amounted to approximately Rs 24.24 billion.

The weekly total indicates active securities trading, but it does not represent equity transactions alone. NEPSE turnover includes ordinary shares, mutual-fund units and corporate debentures.

Debt securities featured prominently among the highest-turnover instruments during the week.

On Wednesday, the 11 percent KBL Debenture 2089 recorded transactions worth Rs 623.9 million, the highest turnover of the session. Global IME Bank Debenture 2086/87 topped Thursday’s turnover rankings with transactions worth Rs 355.8 million.

The trend became more visible on Friday, when the 8.5 percent Nepal Bank Debenture 2087 led the market with turnover of approximately Rs 899.1 million.

Debenture trading is a legitimate and important part of the capital market. A more active debt market can improve liquidity and provide investors with alternatives to ordinary shares.

However, debt-security transactions should not be treated as evidence of an equivalent increase in demand for equities.

Friday’s Rs 6.86 billion turnover therefore reflected activity across different classes of securities. The figure cannot be interpreted as Rs 6.86 billion of buying and selling in listed company shares.

A clearer assessment of equity participation would require separate data on ordinary-share turnover, the distribution of transactions across listed companies and the degree to which activity was concentrated in a limited number of securities.

The Securities Board of Nepal added a new policy dimension to the market on July 9.

SEBON said it had taken serious note of problems in the capital market and grievances raised by investors. The regulator announced that it would publish a detailed, time-bound capital-market development roadmap the following week and begin its implementation immediately.

The announcement also referred to the effective implementation of margin trading and a review of the Securities Act, securities-registration and issuance regulations, and corporate-governance guidelines for listed companies.

Licensed securities businesses and related institutions were directed to complete their assigned responsibilities within specified periods.

SEBON’s announcement formally acknowledged concerns surrounding the market and placed a timetable on the proposed reform programme.

The significance of the announcement will depend on the contents of the roadmap.

A credible plan would need to identify specific measures, implementation deadlines, responsible institutions and mechanisms for monitoring progress. It would also need to distinguish reforms that can be implemented administratively from those requiring legal amendments, technological development or coordination among multiple agencies.

The roadmap’s publication will therefore be the beginning of the assessment rather than the completion of reform.

SEBON’s announcement was issued after Thursday’s trading session.

Thursday’s 19.67-point decline preceded the public statement and cannot be described as a market reaction to the proposed roadmap.

Friday was the first trading session following the announcement. The index closed 1.13 points lower after fluctuating between 2,592.67 and 2,623.24.

A single near-flat session offers insufficient evidence to determine how the market evaluated the announcement. The response will become clearer only after the roadmap is published and its measures can be examined in detail.

The market’s reaction will also depend on whether implementation follows the stated timetable.

Alongside the roadmap announcement, SEBON urged investors not to rely on rumours, misleading statements or unverified information.

The regulator advised investors to make decisions based on their own study and analysis while considering their individual capacity to bear risk.

The warning is relevant to a market in which expectations surrounding policy changes can affect sentiment before official measures are finalised.

Discussions about margin trading, public offerings, regulatory amendments or market-support measures can generate expectations before their practical effects are known. Proposals may begin circulating as if they were approved policies, while preliminary discussions can be presented as final decisions.

SEBON’s roadmap could provide an important basis for capital-market reform. Its publication alone, however, will not automatically improve surveillance, disclosure standards, margin-trading facilities, enforcement or investor protection.

Those changes will depend on the quality and execution of the measures announced.

The description of confidence as fragile rests on the market’s lack of continuity during the week.

NEPSE rose on Tuesday, but the gain was fully erased on Wednesday. The index then recorded two additional negative sessions and ended the week close to 2,600.

The weekly movement does not measure the intentions or emotions of individual investors. It does show that the positive session did not develop into a broader multi-day advance.

A more convincing recovery would require gains to extend across several sessions, participation to broaden across sectors and equity turnover to strengthen beyond activity concentrated in individual instruments.

Listed companies’ financial performance will also remain important. Earnings, cash flow, asset quality and operating conditions provide a stronger basis for evaluating whether rising share prices are supported by underlying business performance.

Regulatory progress will form another part of that assessment. SEBON’s roadmap will be judged on its content, timetable and implementation rather than on the announcement alone.

The July 6–10 trading week should not be interpreted as proof of either a sustained bear market or an imminent recovery.

NEPSE recorded one positive session, but the gain did not continue. Total turnover remained sizeable, but debt securities accounted for a visible portion of activity on several days. SEBON promised a time-bound reform roadmap, but its contents had not been published by the end of the week.

The next test will not be defined by a single green session.

It will depend on whether future gains are sustained, whether participation in equities broadens and whether SEBON converts its announced timetable into specific and measurable action.

Until those developments become visible, the market’s capacity to rebound remains evident, but the basis for sustained confidence remains limited.

-22.png)